.webp)

Finding your way through infertility is already hard enough without having to become a legal researcher on your lunch break. It can feel surreal to sit in a waiting room, processing another round of bloodwork or spotting, while also secretly Googling, “Does my state make insurance cover IVF?”

Here is the truth. Infertility care in the United States is a patchwork of policies that depend on your zip code, your employer, and sometimes even your relationship status. For the 1 in 5 women who struggle to get pregnant after a year of trying (according to 2024 data from the CDC), that reality is not only exhausting, it is deeply unfair. One state may offer several covered IVF cycles. Another might only cover diagnostic testing. A few offer nothing at all.

The good news is that the landscape is shifting. More states are adding fertility mandates, IVF costs are better documented than ever, and families are pushing successfully for change. This guide is here to help you understand where your state stands in 2025, what your insurance may be required to do, and how to advocate for yourself if you live somewhere with little or no support.

States that require fertility coverage in 2025

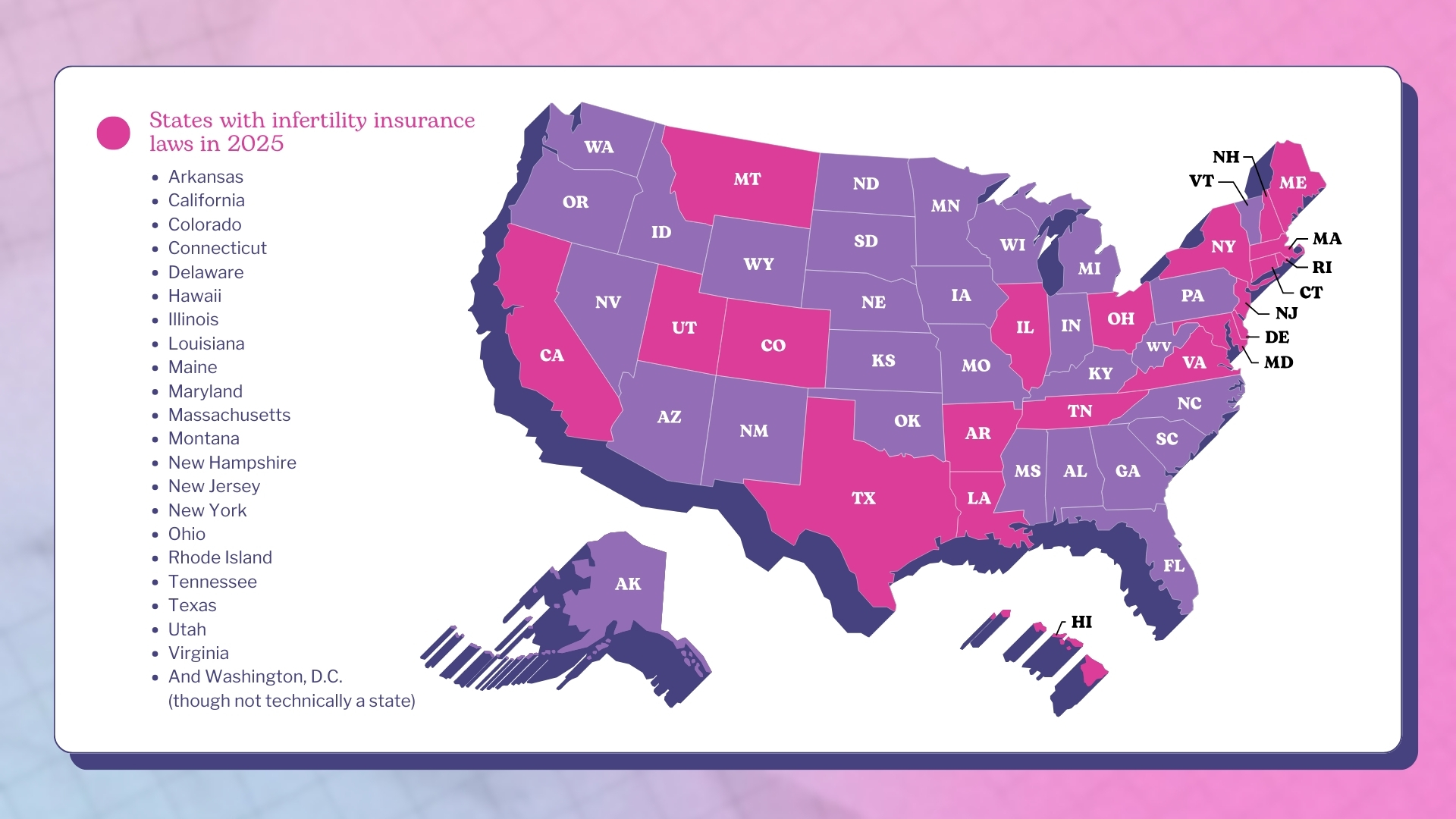

If you are searching for a quick answer, here it is. As of 2025, 22 states have laws related to infertility insurance coverage, although not all require IVF. Some states require insurance companies to cover infertility treatment. Others require insurers to offer plans that include coverage, but employers do not have to pay for them. A handful have infertility mandates that do not explicitly include IVF at all.

Here’s the list of states with infertility insurance laws in 2025:

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Hawaii

- Illinois

- Louisiana

- Maine

- Maryland

- Massachusetts

- Montana

- New Hampshire

- New Jersey

- New York

- Ohio

- Rhode Island

- Tennessee

- Texas

- Utah

- Virginia

- And Washington, D.C. (though not technically a state), which enacted one of the most comprehensive fertility mandates in 2023, requiring coverage for infertility treatment and IVF. This doesn’t apply to all federal plans, but for local residents it can significantly reduce out-of-pocket costs.

Recent legislative changes to know about

A few states have updated or expanded their laws in the last two years:

- Colorado (2023): Strengthened its already robust mandate by clarifying IVF coverage requirements for large group plans.

- Tennessee (2023): Added a mandate to offer IVF coverage, marking a major shift for the state.

- Maine (2023): Fully implemented its infertility coverage law, including IVF provisions.

- Maryland (2024): Expanded coverage to include same-sex couples and donor-related treatments without additional barriers.

- Utah (2024): Expanded infertility treatment coverage and updated rules for fertility preservation.

More states are considering similar moves for 2025 and beyond, and we will cover these in the section on future trends.

Understanding state-mandated fertility coverage

State-mandated fertility coverage means that state law requires some forms of infertility testing or treatment to be included in certain insurance plans. However, states define infertility coverage in completely different ways.

There are two types of mandates:

Mandate to cover

Insurance companies must include infertility treatment in every plan they sell within that state. Coverage varies, but IVF is often included.

Mandate to offer

Insurance companies must make at least one infertility-inclusive plan available, but employers do not have to buy it. This is common in states like Texas, Tennessee, and Louisiana.

You will also see a wide range of eligibility criteria. Some states require a specific duration of infertility, others set age limits, and some impose restrictions based on marital status or whether you are using donor tissue.

This is why it is so important to understand what your specific state law requires rather than relying on the general claim that a state “covers” infertility.

Fertility coverage by state: What's actually included

Every state handles infertility insurance differently, and the definitions can be surprisingly inconsistent. Below is a simple breakdown of what each state offers in 2025 so you can quickly see whether IVF is covered, partially covered, optional, or unclear.

Arkansas

Arkansas was one of the first states in the U.S. to recognize that infertility care should be treated as essential healthcare rather than an optional add-on. The state’s law requires private insurers to cover IVF for eligible patients, although cycle limits and medical requirements may apply. This early legislation has helped many families access treatment who otherwise would not have been able to afford it.

- IVF covered

- Mandate to cover

- One of the earliest states to require IVF coverage

California

California has long required insurers to offer at least one plan with infertility benefits, but IVF remains excluded by law. This means patients in California may have coverage for diagnostics or medications, but full ART services like IVF require self-payment unless an employer voluntarily adds coverage.

- IVF not covered

- Mandate to offer

- Insurers must offer at least one plan with infertility coverage, but IVF is excluded

Colorado

Colorado is often described as one of the most progressive states in the country when it comes to fertility care. Its mandate requires coverage of diagnosis, treatment, and IVF, along with fertility preservation for medically induced infertility. The law also includes protections for same-sex couples and single parents.

- IVF covered

- Mandate to cover

- One of the strongest and most inclusive mandates in the country

Connecticut

Connecticut’s infertility mandate includes fairly comprehensive coverage, including IVF, IUI, and diagnostic testing. While there are medical criteria and lifetime maximums, the state remains one of the leaders in making treatment financially accessible.

- IVF covered

- Mandate to cover

- Includes coverage for multiple cycles with medical criteria

Delaware

Delaware’s fertility mandate includes a wide range of services, such as IVF and fertility preservation for medically induced infertility. The law is considered one of the more modern and inclusive mandates, reflecting current ART standards.

- IVF covered

- Mandate to cover

- Includes fertility preservation for medically induced infertility

Hawaii

Hawaii was an early adopter of IVF coverage, requiring insurers to cover at least one IVF cycle for eligible married couples using the patient’s own sperm and eggs. The law is more restrictive than in some states, but it still provides significant relief from high out-of-pocket costs.

- IVF covered

- Mandate to cover

- Covers one cycle for eligible patients

Illinois

Illinois offers one of the most comprehensive fertility mandates in the United States. The law requires IVF coverage, includes donor eggs and sperm, and provides broad protections for different family-building paths, including same-sex couples.

- IVF covered

- Mandate to cover

- Comprehensive coverage that includes donor tissue

Louisiana

Louisiana requires insurers to offer plans with infertility benefits, but IVF is explicitly excluded by statute. Patients may receive coverage for diagnostic testing or certain treatments, but IVF costs are out-of-pocket unless an employer voluntarily adds coverage.

- IVF not covered

- Mandate to offer

- State law explicitly excludes IVF

Maine

Maine’s infertility law became fully effective in the last few years and now includes coverage for IVF, donor tissue, and fertility preservation. The update brought the state in line with some of the stronger mandates across the country.

- IVF covered

- Mandate to cover

- Recently expanded to include more comprehensive ART benefits

Maryland

Maryland’s fertility mandate includes IVF coverage, diagnostic testing, IUI, and fertility preservation. In 2024, Maryland expanded the law to include same-sex couples and individuals using donor tissue, removing earlier barriers that required heterosexual intercourse for eligibility.

- IVF covered

- Mandate to cover

- Expanded in 2024 to ensure coverage for same-sex couples and donor use

Massachusetts

Massachusetts consistently ranks among the top states for infertility coverage. The mandate requires coverage for IVF and a wide range of ART services without the narrow restrictions seen in other states. Many patients in Massachusetts pay only small copays for treatments that cost tens of thousands elsewhere.

- IVF covered

- Mandate to cover

- Considered one of the strongest and most equitable mandates in the U.S.

Montana

Montana requires insurers to offer coverage for infertility treatment, but does not specify whether IVF must be included. Because the statutory language is vague, IVF coverage varies significantly between insurers and employer plans.

- IVF coverage unclear

- Mandate to offer

- Law requires insurers to offer infertility treatment, but IVF is not specified

New Hampshire

New Hampshire requires insurers to cover a wide range of infertility treatments, including IVF, diagnostic testing, and other ART procedures. The state’s law is comprehensive and supports many different treatment pathways.

- IVF covered

- Mandate to cover

- Coverage includes diagnostic testing and ART

New Jersey

New Jersey mandates coverage for IVF and other infertility treatments, but includes specific criteria such as age limits, medical testing requirements, and a definition of infertility that some consider restrictive. Even so, the mandate remains one of the more helpful in the country.

- IVF covered

- Mandate to cover

- Some restrictions apply, such as age limits and prior testing

New York

Questions Women Are Asking

New York requires large-group insurance plans to cover up to three IVF cycles. The law also expanded coverage for fertility preservation and broadened the definition of infertility to support more inclusive family-building options. Small-group and individual plans may not have the same requirements.

- IVF covered for large-group plans

- Mandate to cover

- Requires coverage for up to three IVF cycles for eligible enrollees

Ohio

Ohio has a mandate requiring insurers to cover infertility treatment, but the law does not explicitly mention IVF. As a result, IVF coverage varies widely. Many plans cover diagnostic testing and medications, but exclude IVF unless employers add it voluntarily.

- IVF coverage unclear

- Mandate to cover infertility treatment

- Law references infertility services but does not explicitly include IVF

Rhode Island

Rhode Island requires insurers to cover infertility treatment and IVF, including multiple cycles within a defined lifetime maximum. The state has one of the most generous lifetime coverage limits in the country.

- IVF covered

- Mandate to cover

- Includes multiple IVF cycles with specific lifetime maximums

Tennessee

Tennessee introduced a fertility coverage law in 2023 that requires insurers to offer plans with IVF benefits. The law does not require employers to purchase these plans, so coverage varies. Still, it marks a significant shift for a state that previously offered no infertility protections.

- IVF covered

- Mandate to offer

- New law introduced in 2023 requires insurers to offer IVF-included plans

Texas

Texas requires insurers to offer plans with IVF benefits, but the eligibility criteria are among the strictest in the country. Patients must meet specific medical definitions of infertility, and there are requirements around marital status and the use of the couple’s own genetic material.

- IVF covered in limited circumstances

- Mandate to offer

- Coverage only applies in very specific, medically defined scenarios

Utah

Utah recently expanded its infertility benefits, but IVF coverage varies significantly between plans. Some patients have access to diagnostics or fertility preservation without ART coverage. The law is improving, but IVF requirements remain inconsistent.

- Partial fertility coverage

- Mandate to cover

- IVF coverage depends on the plan and is not always required

Virginia

Virginia requires certain insurance plans to cover infertility treatment, including IVF. However, the mandate does not apply to all plan types, so access can still vary depending on the employer and the insurer.

- IVF covered for eligible plan types

- Mandate to cover

- Includes IVF but may not apply to all insurance markets

Washington D.C.

Washington D.C. introduced a comprehensive fertility mandate in 2023 that requires insurers to cover infertility treatment and IVF. The mandate includes inclusive definitions of infertility, coverage for donor tissue, and fertility preservation. Federal employee plans within D.C. may follow different rules, but local coverage is strong.

- IVF covered

- Mandate to cover

- Includes treatment, donor services, and fertility preservation

What does state-mandated fertility coverage include?

Every state’s rules are different, but fertility mandates may cover some or all of the following:

- IVF cycles: Some states require a specific number of cycles. For example, New York requires large-group plans to cover up to three cycles, while Hawaii and Rhode Island offer one or more cycles depending on medical need.

- Fertility preservation: This includes egg or sperm freezing for people undergoing medical treatments that may cause infertility. States like Colorado, Delaware, Illinois, Maine, and Maryland include this protection.

- Diagnostic testing: Most states with mandates include testing such as bloodwork, ultrasounds, and semen analysis.

- Egg freezing: This is typically included only when medically necessary, such as before cancer treatment. Elective egg freezing is rarely covered.

- Inclusivity requirements: Some states now explicitly cover same-sex couples, single parents by choice, and people using donor tissue. Maryland and Colorado have been leaders here.

How much does fertility treatment cost with and without insurance?

Based on 2024 data from the US. Department of Health and Human Services, the cost of a single IVF cycle can range from $15,000 to $30,000 for those who are navigating infertility and choose to try IVF.

Insurance can make a dramatic difference. In states with strong mandates, most of the financial burden is absorbed by coverage once a patient meets their deductible and out-of-pocket maximum. Someone living in Massachusetts may only pay a small copay for treatment. In Colorado, a patient might qualify for up to three covered IVF cycles once they have met their initial costs. Meanwhile, a patient in Texas could still face the full price if their employer chose a plan that does not include infertility benefits.

This is why IVF is often described as a lottery based on where you live and the type of insurance your employer offers.

Does your employer have to offer fertility coverage?

Here’s the catch. Even if your state requires insurers to cover infertility treatment, your employer might not be obligated to follow those rules. It all depends on the type of health plan they use.

Fully insured vs self-insured plans

Fully insured plans, which are common among small and medium-sized employers, must follow state laws. If a state mandates infertility coverage, these plans have to include it. Self-insured plans work differently. They are typically used by larger employers, and they follow federal law rather than state mandates. This means they are not required to offer any fertility coverage at all, even if the state has strong protections in place. Because of this gap, many larger employers have started adding fertility benefits voluntarily to help with recruitment and retention.

Read more: Companies That Offer Fertility Benefits

Federal employee benefits (FEHB)

Federal employees have seen a significant expansion in fertility benefits in recent years. As of 2024, more than 20 FEHB plans offer IVF coverage, fertility preservation, and multiple cycles of ART. This marks one of the biggest federal improvements to fertility coverage to date and has made treatment more accessible for many government workers and their families.

Military benefits (TRICARE)

TRICARE provides fertility preservation for service members whose infertility is caused by a service-related injury, along with IVF for those who meet strict eligibility criteria. Coverage for spouses depends on the specific situation and often requires approval through military medical centers, but the system has become more supportive in recent years as awareness of service-connected infertility grows.

Marketplace and self-employed plans

Infertility is not considered an essential health benefit under the Affordable Care Act. This means marketplace plans are not required to include fertility coverage unless a state mandates it. If you are self-employed and live in a state with a mandate to cover, your marketplace options may be relatively strong. In states without mandates, however, marketplace plans rarely include meaningful fertility benefits, and coverage gaps are common.

How to access your state's fertility benefits

Finding out what you are entitled to takes persistence, but it is absolutely possible. The system is confusing on purpose, which means most people have no idea what their plan truly covers until they are already knee-deep in appointments and bills. You deserve clarity long before that point. With the right questions, the right paperwork, and a little confidence in your corner, you can uncover benefits you did not even know you had and make a real difference in what you end up paying.

- Look up your state's mandate: Use RESOLVE’s state-by-state database to find the exact rules for where you live.

- Read your Summary of Benefits and Coverage: Look for terms like infertility treatment, ART services, IVF, and fertility preservation.

- Get documentation: Many insurers require proof of infertility, such as a diagnosis from your doctor, records of testing, or proof that you’ve been trying to conceive for a certain amount of time.

- Ask your HR team for your plan type: Don’t assume your employer’s plan follows state law. Ask whether your plan is fully insured or self-insured.

- Appeal if you’re denied: Insurance companies deny claims frequently. A well-documented appeal, along with support from your doctor, can make a real difference.

What if your state doesn't mandate fertility coverage?

Living in a state without mandated fertility coverage can feel discouraging, but it does not mean you are out of options. There are still real, practical pathways that can help ease the financial burden and open doors to treatment. Many people build their family this way, and you deserve to know what is available to you.

Grants

A number of nonprofit organizations offer grants specifically for fertility treatment. Groups like RESOLVE, Baby Quest, and the Cade Foundation award funding several times a year to help cover the cost of IVF, medications, and even travel in some cases. These grants are competitive, but they are a lifeline for many families who would otherwise never be able to move forward. The application process takes time, but it can absolutely be worth it.

Financing

Most fertility clinics now offer in-house financing or partner with third-party lenders who specialize in IVF loans. Some clinics also bundle services into treatment packages that can lower the overall cost compared to paying cycle by cycle. Financing is not the right fit for everyone, but it can make treatment more manageable by spreading payments out over time and reducing the immediate financial pressure.

Employer advocacy

If your employer does not offer fertility coverage, you can ask them to add it. More companies are realizing that fertility benefits help with hiring, retention, and employee morale. Many of the plans you see on “best fertility benefits” lists were added because one employee spoke up. You do not need to make a personal disclosure unless you want to. You can simply frame it as a request for inclusive healthcare benefits. Employers often start exploring options after learning that people care about it.

Medical tourism

Some patients choose to travel for more affordable fertility care. This can mean going to a lower-cost clinic in another U.S. state or pursuing treatment internationally where IVF is significantly cheaper. Medical tourism requires careful research and planning, and it is not the right option for everyone, especially if frequent monitoring is needed. Still, many families find that travel opens up possibilities they cannot access at home, and some clinics now offer coordinated care to support out-of-town patients.

The future of fertility coverage in the U.S.

Momentum is building. Several states are actively considering new fertility mandates or expansions, including Pennsylvania, Oregon, Minnesota, North Carolina, and Florida.

There is also growing pressure at the federal level for standardized fertility coverage. Bills have been introduced proposing national infertility coverage requirements, expanded FEHB benefits, and protections for LGBTQ+ family building.

The cultural conversation has shifted. Fertility care is finally being seen as essential health care rather than a luxury.

You deserve access to fertility care. Here's how to fight for it.

Infertility is not a personal failure, and it should not be a financial punishment. The fact that your access to treatment depends on your state, your employer, or your marital status is not fair, and you are absolutely allowed to feel frustrated by that. The system should support you, not add another barrier.

The landscape is changing, though. States are adding mandates. Employers are expanding benefits. Federal employee plans are covering IVF at record levels. People are speaking up, advocating, and winning.

Wherever you live, you deserve real options, real support, and real pathways to parenthood. Keep asking questions, keep advocating for your care, and keep reminding yourself that you are not alone in this. Change is already happening, and your voice matters in building what comes next.

.jpeg)

.jpeg)

.jpeg)

.png)

.png)